Key Takeaways:

If 2021 was known as the year of the beauty dealmaking boom, 2025, by comparison, marked the industry’s recalibration.

That was the clear message from BeautyMatter’s Business Briefing webinar, where investors, bankers, and industry insiders gathered to unpack the forces shaping beauty and wellness investment in 2026. Deal activity slowed last year, but the category's underlying momentum remains strong. What’s changed is not the appetite for beauty but its level of scrutiny.

“The story of 2025 isn't a contradiction,” said BeautyMatter co-founder and President John Cafarelli. “It’s precision.”

BeautyMatter tracked 263 transactions in 2025, down 11.5% year over year, but the decline in volume masks a more nuanced reality: The deals that did happen were larger, more strategic, and executed with far greater discipline. If investor sentiment is any indication, that discipline is here to stay.

Optimism with Sharper Pencils

Despite macroeconomic noise and a valuation reset, the mood among beauty dealmakers remains overwhelmingly positive.

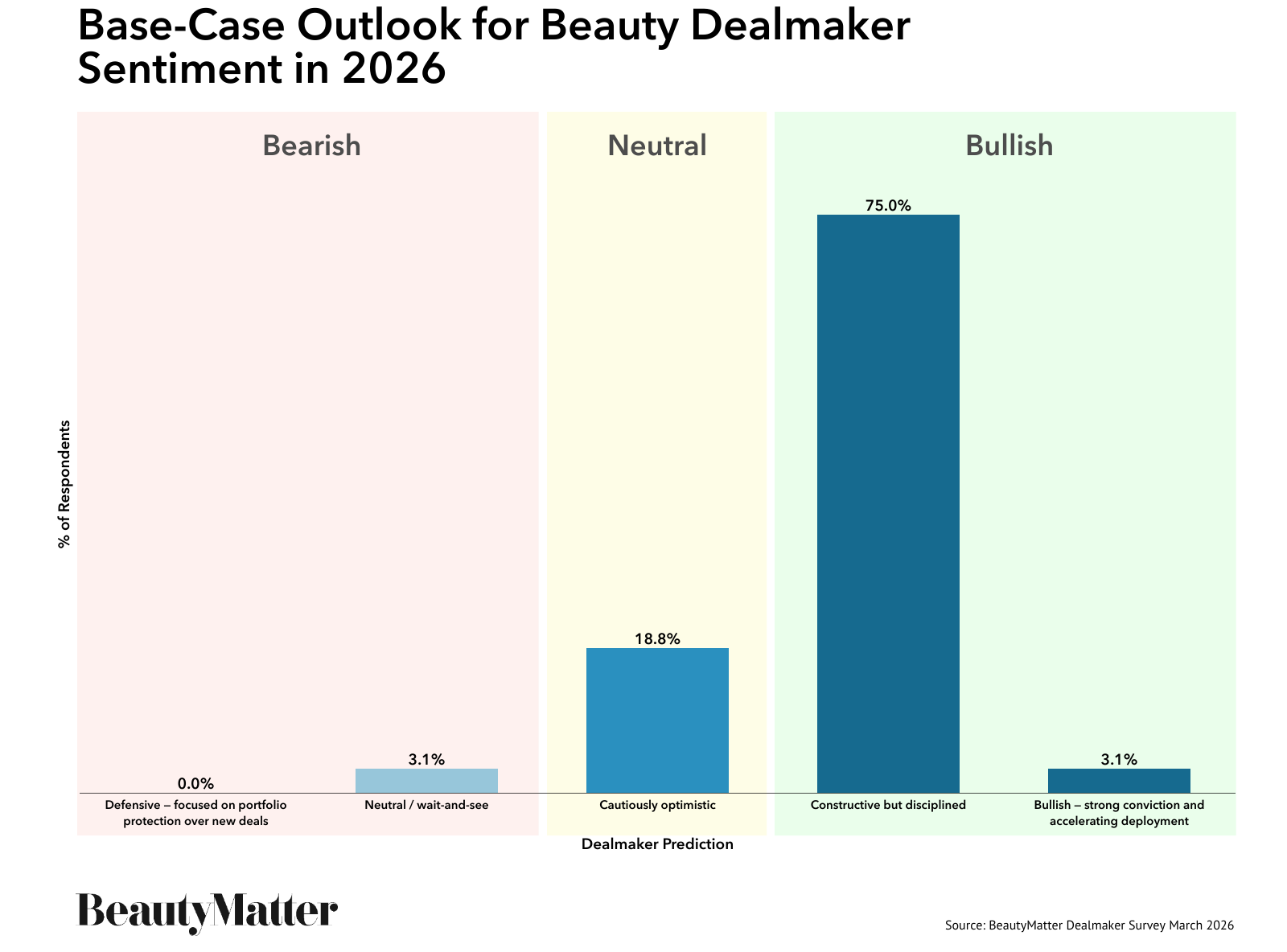

Nearly 78% of respondents to BeautyMatter’s dealmaker sentiment survey described the outlook for 2026 as either “constructive but disciplined” or outright “bullish,” signaling broad confidence in the resilience of beauty and wellness as investment categories.

In fact, 75% of respondents described themselves as "consultative but disciplined,” while another 3% said they were bullish with strong conviction and accelerating capital deployment. No respondents indicated they were adopting a defensive stance.

In other words, capital remains available but far more selective.

The biggest barriers to dealmaking today are not tariffs or consumer demand. Instead, investors point to a widening gap between buyer and seller expectations, a lingering consequence of the frothy valuations seen earlier in the decade.

More than 81% of dealmakers cited valuation disconnects between buyers and sellers as the biggest constraint to transactions, while 78% pointed to limited exit opportunities from strategics or large private equity firms.

For Rich Gersten, co-founder and Managing Partner of True Beauty Ventures, that recalibration was inevitable. “Valuation expectations peaked in 2021. Things are getting more rational now. But founders and investors still need to meet somewhere in the middle.”

Gersten emphasized that his firm remains bullish on beauty and wellness, but increasingly focused on fundamentals. “Velocity without margin is fragile. Profitability without growth isn’t interesting.”

The Brands That Win Capital

What investors want from beauty brands has also evolved. During the investor panel, Alicia Sontag, co-founder and Managing Partner at Prelude Growth Partners, described the shift away from the growth-at-all-costs mentality that once defined the category.

Prelude’s portfolio includes category-defining brands like Sol de Janeiro, which the firm backed in 2019, leading to its explosive global growth. For Sontag, the lesson from those successes is simple: Brands that endure are built on substance.

“What we’re really looking for are the brands that will be category leaders decades from now,” Sontag said. “That starts with an authentic founder, a product that is meaningfully differentiated, and the ability to generate buzz disproportionate to the size of the business.”

In that framework, the financials are less the starting point than the outcome. “The P&L is really just a financial representation of the strength of your brand,” Sontag explained. “If the product is truly differentiated and people are obsessed with it, the economics follow.”

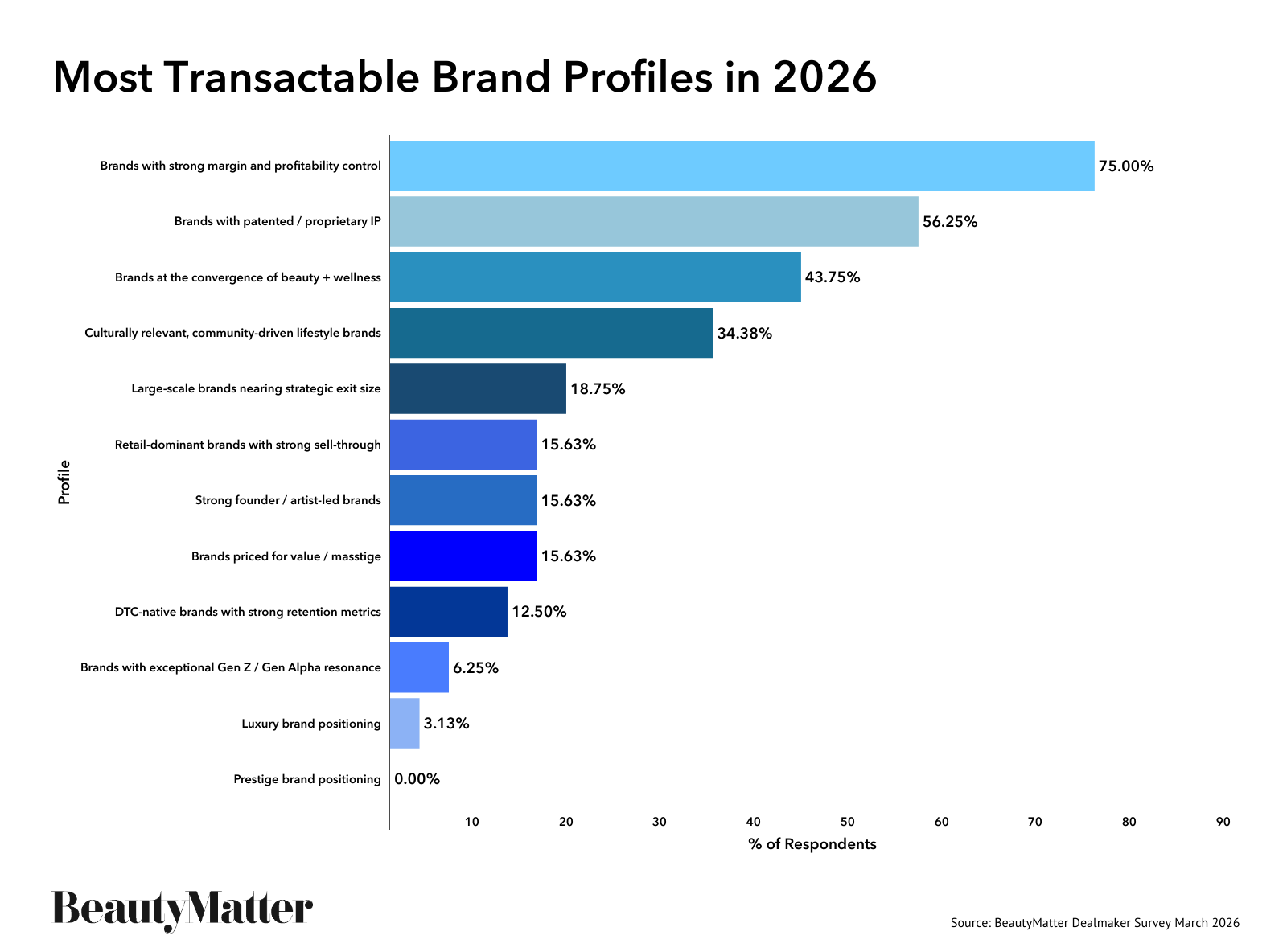

Survey data reinforced that perspective. Seventy-five percent of investors said the most attractive brands are those with strong margins and control over profitability, while 56% prioritize brands with proprietary or patented intellectual property.

Notably, brands positioned at the intersection of beauty and wellness ranked third, cited by nearly 44% of respondents—a signal of where the next wave of opportunity may lie.

A More Competitive Landscape

Even as a capital remains interested in beauty, breaking through has become more difficult.

Sontag pointed to the increasingly crowded competitive environment and the growing complexity of distribution as two defining forces shaping the market.

“Beauty and wellness are wonderful categories because they have long-term growth,” she said. “But every year they also become more competitive.”

That competition now comes from everywhere—from legacy brands and emerging indie players to the resurgence of K-beauty brands.

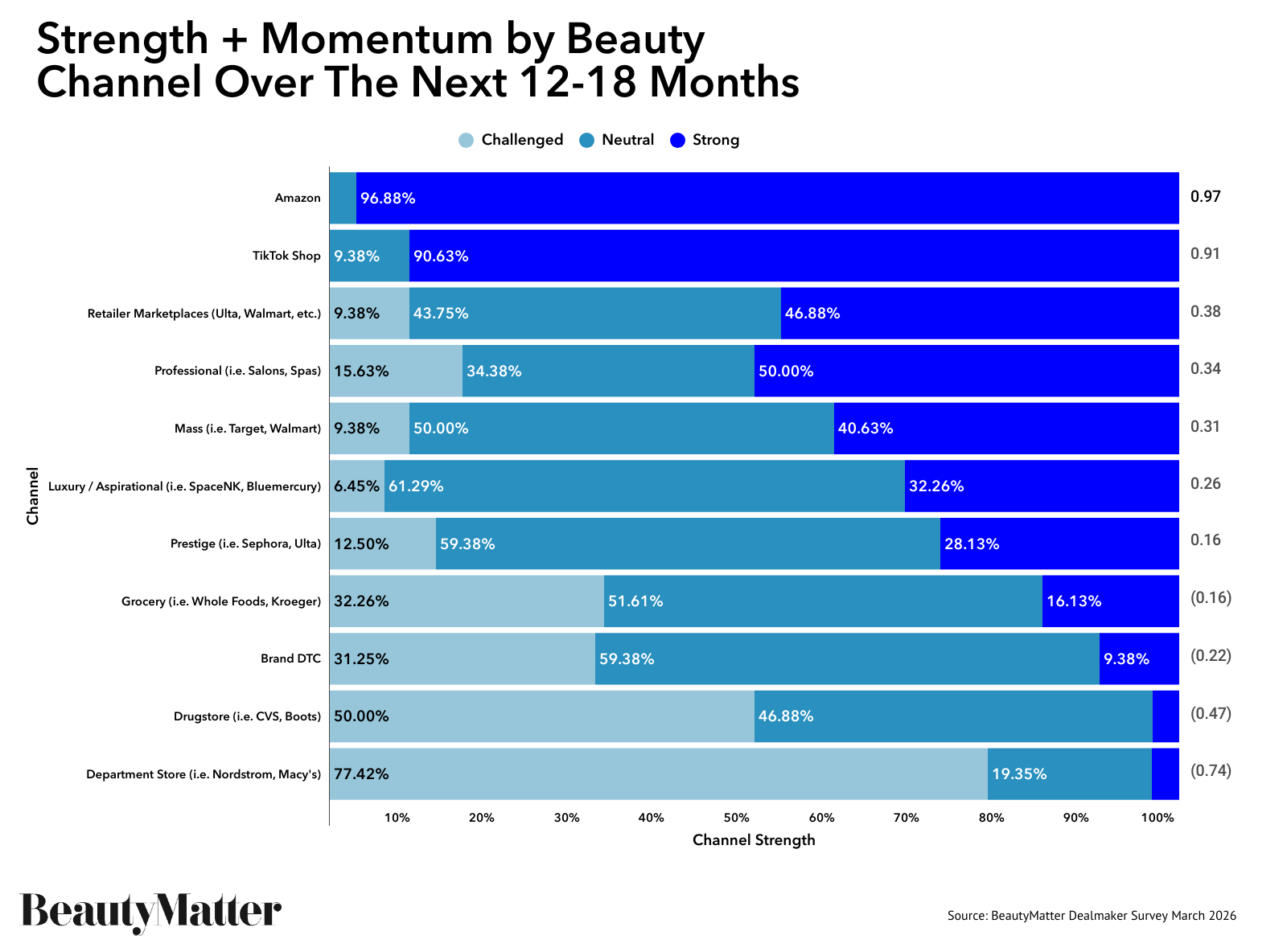

Distribution has also been reshaped dramatically.

According to the survey, Amazon and TikTok Shop rank as the two channels with the strongest growth momentum for beauty over the next 12-18 months, with 96.9% and 90.6% of respondents, respectively, rating them highly.

Traditional channels are more mixed. Prestige retail remains stable, but department stores—historically the backbone of luxury beauty distribution in the US—ranked as the weakest channel in the survey.

Sontag believes successful brands will need to build leverage across multiple channels rather than rely on any single retail partner. “The brands we invest in have power beyond their channel. Retail should amplify the brand, not define it,” Sontag added.

The Convergence of Beauty and Wellness

If there was one theme that surfaced repeatedly throughout the briefing, it was the convergence of beauty and wellness.

Investors increasingly view ingestible, clinical skincare, devices, and functional health products as part of the same consumer mindset.

Gersten described the trend as expanding the opportunity set for investors. “The convergence of beauty and wellness increases the addressable market for us.”

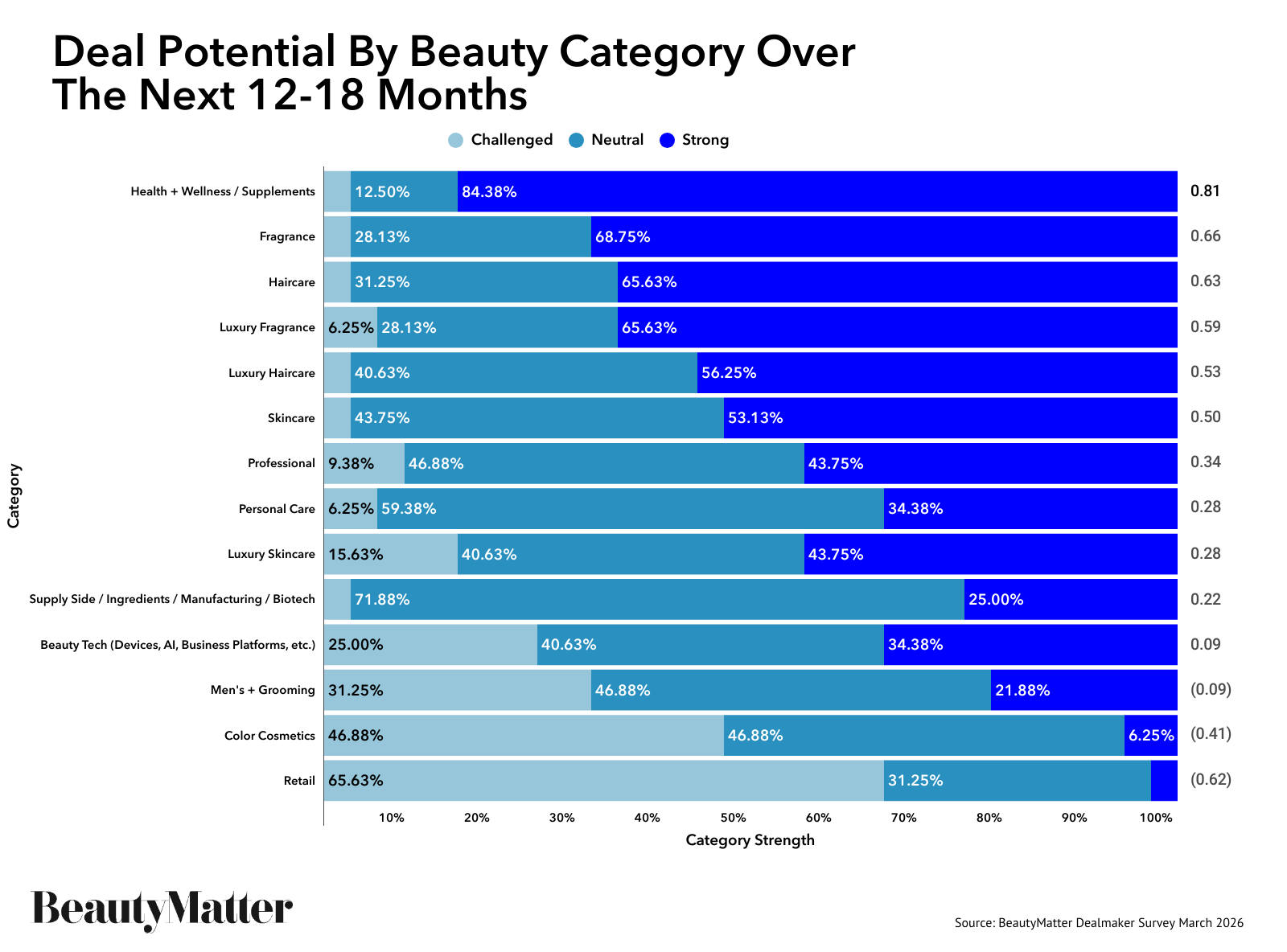

Survey data reinforces that momentum. Health and wellness supplements ranked as the category with the strongest deal potential over the next 12-18 months, followed by fragrance and haircare.

But the trend also introduces new complexities. During the banker roundtable, Ilya Seglin, Managing Director at Cascadia Capital, cautioned that brands entering wellness categories must prove they own something truly defensible.

“Investors have seen a lot. The question is whether the brand actually owns something proprietary," Seglin explained.

At the same time, convergence could expand the universe of potential acquirers.

According to Sasha Radic, Managing Director at Jefferies, wellness-oriented beauty brands may appeal to companies outside traditional cosmetics conglomerates.

“It expands the buyer universe. You start bringing in players who are comfortable with those technologies—pharma-adjacent companies, OTC players, broader CPG companies.”

Still, not every potential acquirer is ready to embrace ingestible products. “Some strategics are comfortable with products that go on the skin,” Seglin noted. “They are less comfortable with products that go in the mouth.”

The Market Ahead

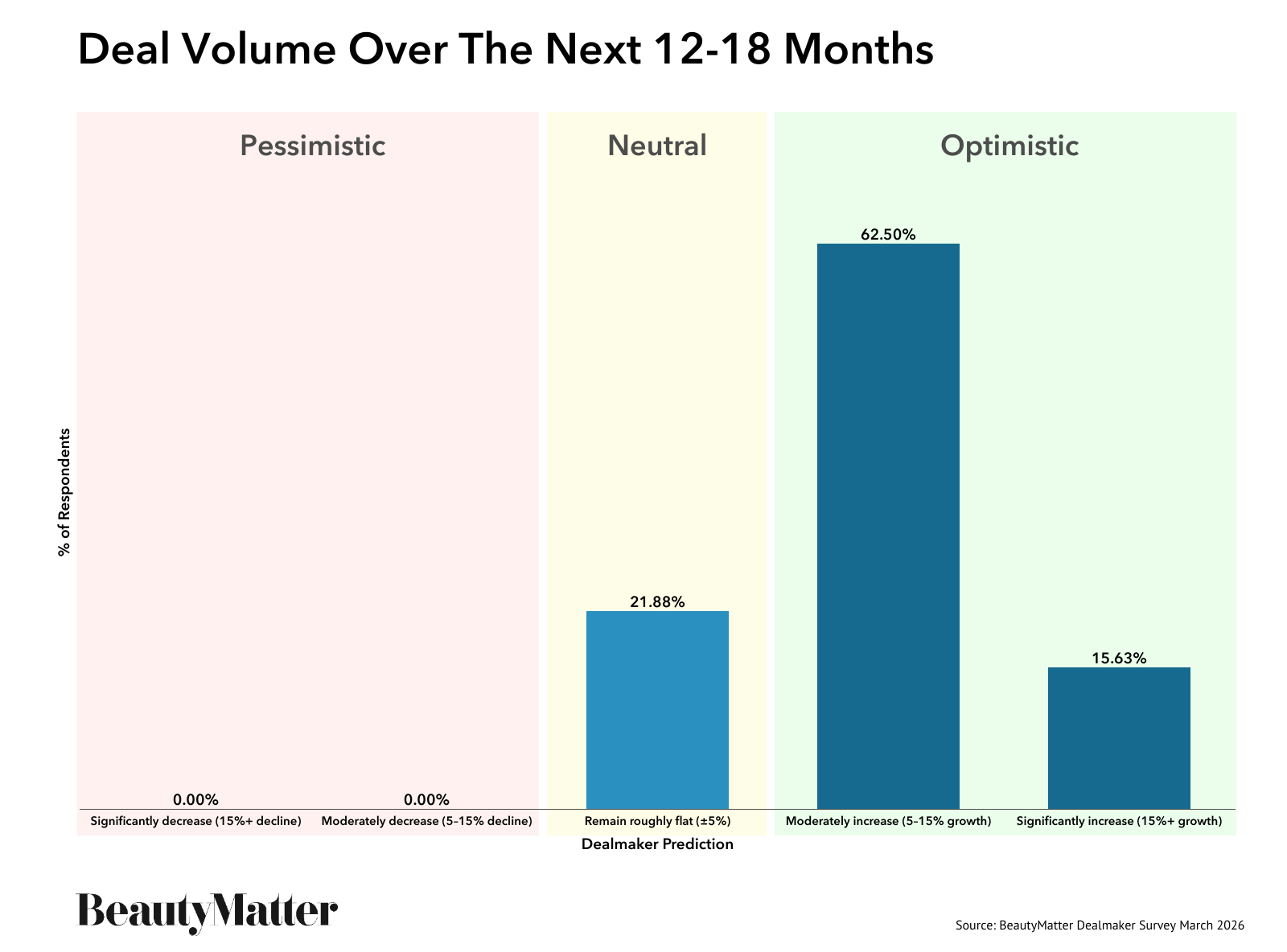

Looking forward, dealmakers expect activity to increase modestly over the next 12-18 months. More than 62% of survey respondents expect deal volume to increase moderately, while another 16% expect it to increase significantly.

At the same time, 56% believe valuation multiples will remain stable, suggesting the market has settled into a new equilibrium after several volatile years.

But the biggest shift may be philosophical. The era when marketing hype alone could command premium valuations appears to be over. Investors now want brands that can demonstrate lasting relevance, strong unit economics, and a credible path to profitability.

For Sontag, that shift ultimately strengthens the industry. “Beauty and wellness have grown confidently for decades. The opportunity is still enormous—but the brands that succeed will be the ones with real substance behind them."

In other words, beauty dealmaking hasn’t slowed; it's grown up. As the industry enters its next chapter, discipline may prove to be its most valuable asset.